As India’s private wealth expands, Raja Mukherjee’s research perspective places the country’s private banking future in a larger Asian and global context, comparing India with established wealth centres while arguing for a new financial architecture built around GIFT City, AI-led advisory, structured finance and family-office governance.

Next-Generation Private Banking Excellence is becoming one of the most important financial conversations in India as UHNW wealth, family offices, GIFT City, AI-led advisory and structured finance begin reshaping the country’s private banking architecture.

India is no longer merely a high-growth economy producing new wealth. It is becoming a financial civilisation in transition, a country where entrepreneurial capital, family-business succession, public-market depth, private-market ambition and global Indian mobility are converging at the same time.

This is the larger context in which Raja Mukherjee’s research perspective becomes relevant. His thesis does not treat private banking as a narrow wealth-management service. It frames private banking as part of India’s next financial architecture: a system that must serve ultra-high-net-worth individuals, family offices, corporate promoters, founders, institutions and globally mobile Indian capital.

For decades, Indian private banking largely operated as a relationship-led distribution business. The private banker was a trusted contact, a product facilitator, a discreet adviser and, often, a bridge between a wealthy family and investment opportunities.

That model is no longer enough.

India’s wealth has become more complex. Its capital is more global. Its families are more sophisticated. Its entrepreneurs compare domestic service standards with Singapore, Dubai, Zurich, London, New York and Hong Kong. The question is no longer whether India has wealth. The question is whether India can build a private banking and structured finance ecosystem worthy of that wealth.

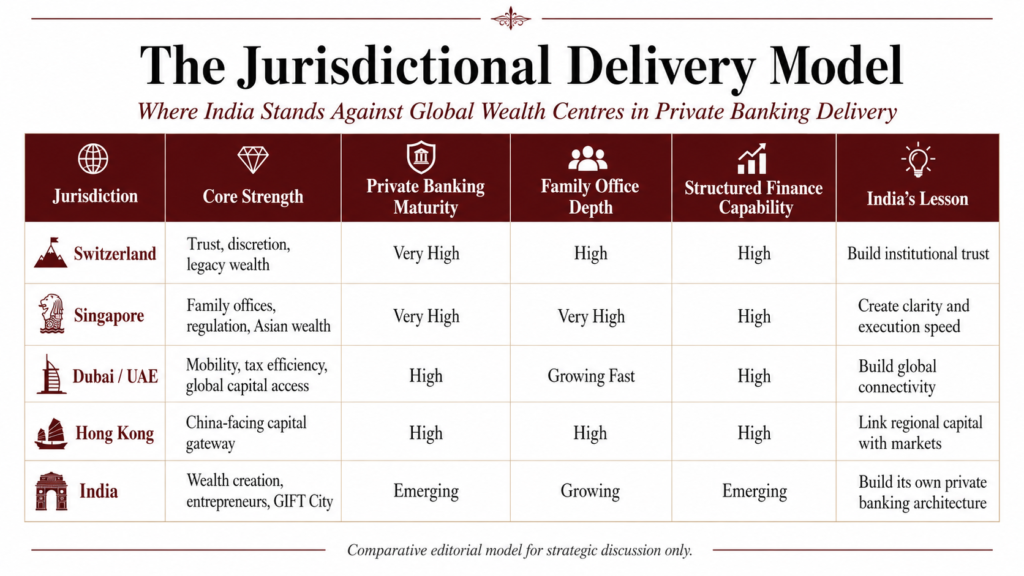

India’s Wealth Moment in the Asian Context

Across Asia, private banking has matured around different models.

Singapore has built itself into a highly trusted family-office and asset-booking centre, supported by regulatory clarity, global banking presence, political stability and a deep international adviser ecosystem. Hong Kong has long served as a gateway to Chinese and North Asian wealth, though its positioning has evolved with geopolitical and market shifts. Mainland China has produced enormous private wealth, but its wealth-management model remains closely shaped by domestic regulatory priorities. Japan has deep institutional capital and inheritance complexity, but a slower wealth-growth profile compared with emerging Asia.

India is different.

India’s private wealth story is still in acceleration. The country’s UHNWI base is large but still has a long runway compared with more mature wealth economies. Its entrepreneurs are younger. Its domestic markets are deepening. Its family businesses are passing through generational transition. Its technology founders, listed-company promoters, professional executives and family offices are all becoming more financially sophisticated at the same time.

This makes India one of Asia’s most important private banking opportunities. But it also creates a challenge: India cannot simply import another country’s model.

Singapore’s strength is international wealth administration. Switzerland’s strength is discretion, legacy and multi-generational preservation. Dubai’s strength is mobility, tax efficiency, global connectivity and lifestyle-linked capital. Hong Kong’s strength has historically been China-facing capital access. The United States offers scale, innovation and private-market depth.

India must build something different: a domestic-global wealth architecture rooted in Indian enterprise, Indian regulation, Indian families and Indian capital ambition.

Why India Must Not Simply Copy Singapore, Dubai or Switzerland

It is tempting to say India should become the next Singapore or the next Switzerland. That is too small a vision.

India’s private wealth is not identical to Swiss wealth or Singaporean wealth. Much of Indian wealth is promoter-led, operating-business-linked, family-controlled and emotionally tied to enterprise creation. Indian families often think about wealth alongside reputation, succession, philanthropy, community standing, real estate, business control and next-generation education.

A Swiss-style custody model alone cannot address this. A Singapore-style booking centre alone cannot address this. A Dubai-style mobility model alone cannot address this.

India needs a model that combines four layers.

The first layer is relationship trust. Indian wealth still values personal understanding, discretion and continuity.

The second layer is institutional advisory. Wealthy families increasingly need structured advice on portfolio construction, succession, tax, philanthropy, estate planning, private markets and risk.

The third layer is digital intelligence. AI, data integration, risk analytics and client-level insights will become essential to serve sophisticated clients at scale.

The fourth layer is global access. Indian capital must be able to move into global markets, private funds, international structures and cross-border opportunities without losing regulatory discipline.

This is where India’s opportunity becomes powerful. It can build a private banking model that is not merely imported, but designed for its own economic civilisation.

GIFT City: India’s Onshore-Offshore Bridge

For decades, Indian global wealth often moved through external centres. Singapore, Dubai, London, Zurich and Hong Kong became natural points of access for international diversification, offshore structures, family-office administration, global funds and foreign-currency exposure.

GIFT City changes the strategic geometry.

As India’s International Financial Services Centre, GIFT City gives India the possibility of building a regulated onshore-offshore bridge inside its own sovereign framework. For private banking and structured finance, this matters deeply.

A serious Indian private banking ecosystem needs more than domestic PMS, mutual funds and AIF access. It needs global fund access, family investment fund structures, offshore banking capability, international insurance, global custody, cross-border succession planning, structured products, private credit and multi-currency investment architecture.

GIFT City can become the platform through which India offers these capabilities without forcing Indian families to rely entirely on external booking centres.

For India, this is not only a financial services opportunity. It is a strategic opportunity. A country with rising global capital should not permanently outsource the architecture of that capital to other jurisdictions.

From Product Distribution to Advisory Depth

The old private banking model was often built around access to products. Relationship managers introduced clients to structured notes, mutual funds, PMS strategies, AIFs, insurance products, credit options and market opportunities.

That approach is now insufficient.

The next-generation Indian client is informed, globally exposed and more demanding. A founder after an IPO does not need generic investment products. A second-generation business heir does not need a basic portfolio pitch. A family office principal does not want opaque fee structures. A corporate promoter does not want wealth advice separated from treasury, business liquidity, debt, succession and global expansion.

The private banker must therefore evolve from distributor to architect.

Advisory depth will become the new differentiator. This means open architecture, transparent fees, stronger due diligence, sharper portfolio construction, genuine alternatives research, family-governance support and better risk conversations.

Private banking excellence will not be defined by how many products a platform can sell. It will be defined by whether it can protect, structure, grow and govern wealth across generations.

AI and the New Relationship Manager

Artificial intelligence will reshape private banking, but not in the way many expect.

The future is not an AI system replacing the private banker. The future is an AI-enabled private banker becoming more intelligent, prepared and responsive.

AI can help relationship managers understand household-level exposure, identify concentration risk, prepare customised portfolio reviews, detect liquidity needs, summarise complex documents, flag suitability concerns, assist onboarding and improve client communication. It can also help institutions manage large, sophisticated client bases without weakening service quality.

But AI in wealth management must be deployed with restraint. UHNWI clients will not tolerate hallucinated advice, inaccurate portfolio interpretation or careless automation. The data layer must be clean. The compliance framework must be strong. Human judgement must remain central.

In this sense, AI is not a replacement for discretion. It is an amplifier of discretion.

India has a special advantage here. Its digital public infrastructure, account aggregation ecosystem, regulatory technology development and fast-growing financial data environment can support a more intelligent private banking system — if institutions build responsibly.

Structured Finance and Private Markets Move to the Centre

India’s wealthiest clients are increasingly looking beyond listed equities and fixed income. Private equity, venture capital, private credit, real assets, infrastructure, pre-IPO opportunities, structured debt and alternative strategies are becoming central to the wealth conversation.

This reflects a deeper change. Much of India’s most meaningful value creation happens before companies reach public markets. Founders, family offices and sophisticated investors want access to that value creation, but they also need due diligence, risk management and liquidity planning.

Structured finance will become equally important. Promoters may need liquidity without losing control. Founders may need diversification after exits. Corporate families may need acquisition finance, debt restructuring, treasury management and hedging. Family offices may need bespoke capital protection, cash-flow planning and global allocation strategies.

This is where private banking must become more technical.

The future winner will not be the institution with the largest product shelf. It will be the institution that can structure intelligently, explain risk clearly and align financial architecture with family and business objectives.

Corporate and Institutional Wealth Cannot Be Ignored

A mature private banking model must also understand corporate and institutional clients.

India’s largest business families do not separate personal wealth from operating companies as cleanly as Western textbooks suggest. Promoter wealth, treasury decisions, operating-company liquidity, pledged shares, family holding entities, trusts, succession plans and investment vehicles are often connected.

This makes corporate onboarding and institutional advisory critical.

Today, complex corporate onboarding can be slow, repetitive and documentation-heavy. Beneficial ownership checks, KYC updates, tax forms, board resolutions, legal entities and risk reviews often create friction. For India to become a serious private banking and structured finance market, these processes must become faster and more intelligent.

AI-enhanced onboarding, beneficial ownership graphs, continuous risk scoring, automated documentation checks and integrated treasury views can materially improve the experience. This is not merely operational efficiency. It is part of trust-building.

The institution that understands a client’s complete financial architecture will own the relationship.

Family Offices and the Governance Question

The rise of Indian family offices is one of the most important shifts in the country’s wealth landscape.

As wealth grows, families need more than investment performance. They need governance. They need decision-making structures, investment committees, family constitutions, next-generation education, philanthropy frameworks, succession clarity and professional reporting.

In Singapore, family offices have become a major part of the wealth ecosystem. In India, the family office market is still developing, but its potential is enormous.

Indian family wealth carries cultural complexity. It is tied to enterprise, legacy, reputation, community, land, philanthropy and emotional continuity. A mature private banking ecosystem must understand this. It cannot treat Indian families as standard global clients with standard global templates.

This is where India can create its own differentiated model: technically modern, globally connected, but culturally intelligent.

The Visionary Leadership Question

The deeper question raised by Raja Mukherjee’s research perspective is not only about private banking. It is about India’s financial leadership.

Can India build a wealth-management ecosystem that competes with Singapore in family-office depth, Dubai in global mobility, Switzerland in trust, the United States in private-market access and London in financial sophistication, while still remaining Indian in structure and purpose?

That is the real opportunity.

India has the wealth creation. It has the entrepreneurs. It has the family businesses. It has the digital infrastructure. It has GIFT City. It has a rising class of globally aware investors. It has the ambition to become a financial power.

What it now requires is institutional courage.

Banks, wealth platforms, regulators, fund managers and advisory firms must stop treating private banking as an elite sales channel. They must treat it as financial infrastructure.

India’s Chance to Build a Global Wealth Standard

India’s private banking opportunity is large, but it is also time-sensitive. Wealthy clients are already comparing Indian institutions with Singapore, Dubai, Zurich, London and New York. They will not wait indefinitely for domestic platforms to mature.

The next decade will decide whether India becomes only a source of wealthy clients for global centres, or whether it becomes a serious wealth centre in its own right.

The answer will depend on execution.

India must build advisory depth, improve onboarding, strengthen family-office capability, use AI responsibly, expand GIFT City’s role, develop structured finance expertise and create a more transparent private banking culture.

Private banking excellence will not come from premium lounges or polished brochures. It will come from daily operating discipline: faster onboarding, sharper advice, cleaner data, deeper governance, transparent fees, stronger risk conversations and global access delivered within a credible Indian framework.

India’s wealth supercycle has already begun.

The task now is to build a private banking model worthy of India’s place in Asia and eventually, in the world.

About the Research Perspective

This article draws from the financial-market research perspective of Raja Mukherjee, whose work examines private banking, structured finance, wealth management, family offices, AI infrastructure, RegTech and India’s emerging financial architecture.